The Unbeatable Market Myth

Why the efficient market hypothesis doesn't need to apply to you.

There are a lot of lazy clichés that get tossed around as unassailable truths. Such statements are some of the lowest forms of human “thought” and are a heavily utilized technique of the midwit class to appear smarter than they actually are.

One of those clichés that (almost) every midwit loves is “No one can beat the market.”

This cliché is based on the economic theory of the efficient market hypothesis or theory (known as EMH or EMT), which broadly states that, assuming all relevant information is public, markets will quickly find the price for an asset at which point there is no reliable way to obtain any outsized gains.

Here again, the midwit will smirk when you question the idea and remind you that the efficient market hypothesis is well accepted among economists and scholars. “Look, here’s a link I found, it must be true!” or increasingly “ChatGPT told me it was legit.”

But zooming in on what it really means, it’s not applicable for the individual investor, and serves only as a vicious advancement of learned helplessness.

The reality is, the market is full of winners, who have beaten the market, and losers, who have not (and of course everything in between).

The efficient market hypothesis appeals to modern leftists and the midwit class (but I repeat myself) because it attributes these differences to random chance rather than intelligence or skill. The fates of the universe selected the winners, and thus there is nothing special about them and we must help those less fortunate.

However, this says little about the actual hypothesis and how, more importantly, what the actual implications are.

Why Individuals Can Beat EMH

But why is the efficient market hypothesis not valid for individuals? There are a few key reasons the theory doesn’t hold for individuals:

Unrealistic Assumptions: one of the main assumptions underpinning EMH is that “all investors have a rational expectation about future market movements.” This is, on its face, pretty ridiculous. Even among institutions, expectations vary widely. Factor in individuals, and this range gets even more broad (and likely less rational on average). Of all these expectations about the future though, some are inherently going to be more realistic, and thus more profitable than others.

Scale: the efficient market hypothesis probably does hold for multi-billion dollar investments (although even then, Warren Buffet’s performance can provide a counterfactual at that scale). But for individual investors this simply isn’t the case. At large scale, inefficiencies draw attention, competitors replicate, and the efficiency goes away (in theory). But any strategy or profile that you personally target could absolutely be a market inefficiency too small or niche for institutional investors to exploit.

Semi-infinite Dimensionality: the efficient market hypothesis considers a simplified reality. It considers a world where, since all data is known, the right answer is clear. That’s definitively not the case with investing. You can run all the machine learning models you want: you are still going to have varying views on what is best because the volume and types of data available are simply too vast.

The Huckster Effect: proponents of EMT will point to the middling performance of hedge funds as an indicator of its validity. They might bleat… “If professionals can’t beat the market regularly, how can you possibly do it?!”But this performance can be better explained by what I’m terming “the Huckster Effect” which is that any sales-related field invites the best talkers who almost always crowd out the best executors. This inevitably results in middling, seemingly stochastic performance when looked at in aggregate, obscuring the subset who do have strategic advantages.

While any one of these factors would invalidate the expansion of EMT to cover individuals, taken together they suggest individuals shouldn’t consider the market a speed limit for investments.

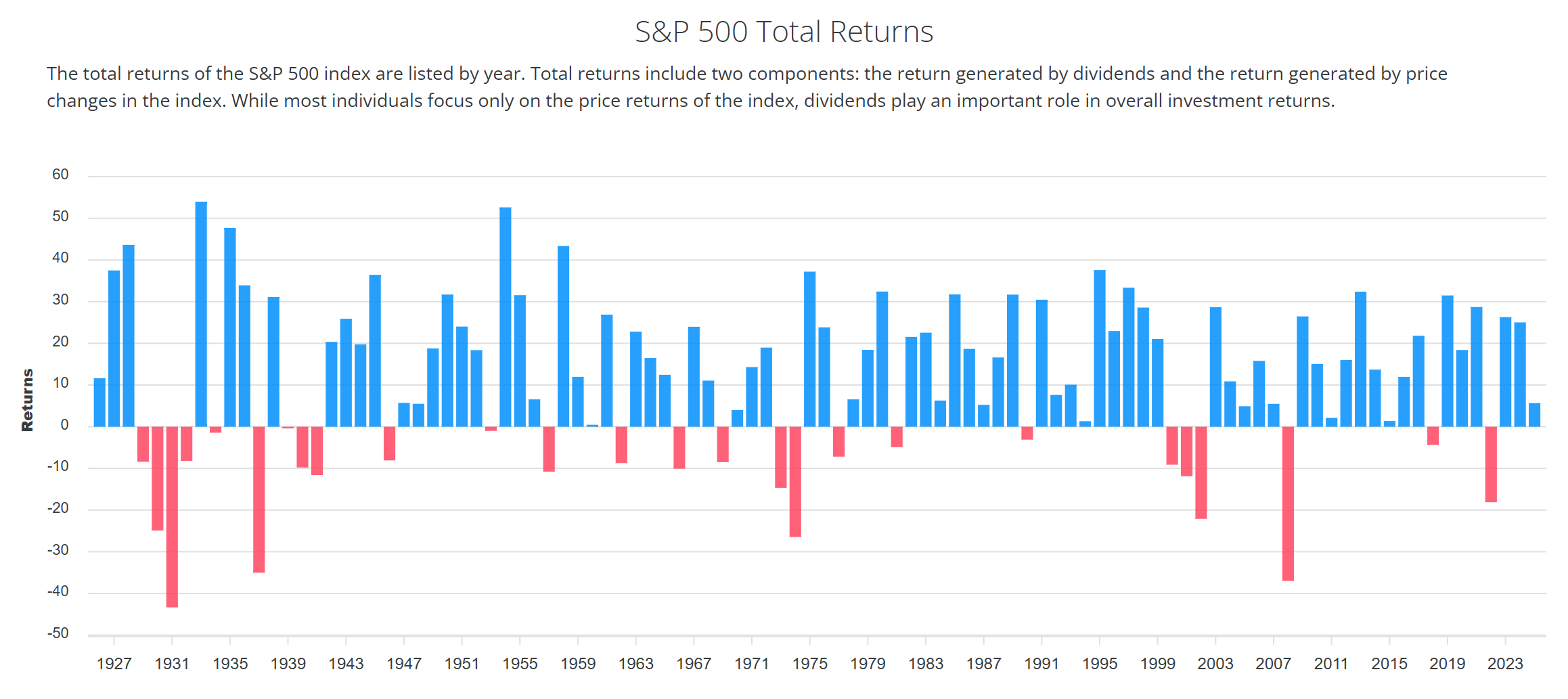

That said, the wisdom of broad market coverage still should hold some weight. Say you were just picking 50 stocks randomly from the S&P 500 to invest in: your return would have the same average as the S&P 500, but with higher variance. Such a strategy is strictly worse than investing in the S&P via VOO or a similar ETF. And if your investment strategy is worse than random, well, the picture dims further.

But on the flip side, there are obvious winning constructs for any given period of time. A thesis around various industries, or even individual stocks can outperform the market. A tech-heavy mix has performed incredibly well over the past 10-15 years, as evidenced by the NASDAQ’s outpacing of the broader S&P index.

But more specific than that, tuned combinations of stocks can have clear market-beating returns for years and even decades at a time. The problem, of course, is finding those investment opportunities and buying them at the right price.

Assuming one is looking at mid-to-long-term investing, this often come down to four things:

Having a cohesive and ultimately accurate prediction of where the world will head over your investment horizon.

Having an effective strategy to derive profit from that future reality.

Tactically executing on that strategy without being too swayed by day-to-day market movements.

Re-evaluating and adjusting your future vision and strategy periodically as the game changes.

These aren’t exactly easy to execute in concert, but it shouldn’t be seen as an insurmountable mountain either. Institutions can be simultaneously overestimated and underestimated. But particularly there can be an overestimated view of hedge funds as filled with brilliant monk-like shamans unswayed by emotion and making perfect decisions in real time.

The reality is that these companies are full of all the same imperfections any human organization faces: politics, ego, saving face, groupthink, and more. Individuals may be at a disadvantage when it comes to total processing power (or the ability to move markets with their moves), but also have advantages of being able to develop a cohesive strategy without any of the messiness of interpersonal dynamics that larger entities must.

I’ll close with a semi-related study on human cooperation between humans and ants:

Watch the video, but the summarized finding is this: ants get much smarter as a group, solving problems that a single ant would not be able to solve. Humans, on the other hand, face challenges communicating and organizing such that group performance of humans “almost never” exceeds the performance of the smartest individual in the group (on this task).

While group human coordination is essential for building many things (due to the scale of what we want to build), running an investment portfolio doesn’t have the constraints that, say, building a company does. As a result, motivated individual investors can (and should) leverage the benefits of working as an individual. By doing so, you can beat the market.